These Five Countries Are Conduits for the World’s Biggest Tax Havens

CAPITALISM, 31 Jul 2017

Javier Garcia-Bernardo, Eelke Heemskerk, Frank Takes and Jan Fichtner – The Conversation

Tax sheltering is not just the domain of exotic Caribbean isles. Major world powers, including the United Kingdom, play a critical and previously undisclosed role in global tax avoidance.

24 Jul 2017 – First came the Panama Papers, then the BahamasLeaks. Journalists continue to shed light on and raise a public outcry over the offshore financial centres that corporations use to reduce their tax bill – something that is still being challenged in court.

A new study has now uncovered all the world’s corporate tax havens and, for the first time, revealed the intermediary countries that companies use to funnel their money into these places.

Published on July 24 in the academic journal Scientific Reports, the paper Uncovering Offshore Financial Centers: Conduits and Sinks in the Global Corporate Ownership Network shows that offshore finance is not the exclusive business of exotic, far-flung places such as the Cayman Islands and Bermuda.

The Netherlands and the United Kingdom also play a crucial – although a heretofore obscure – role in the tax-avoidance game, acting as conduits for corporate profits as they make their way to tax havens.

What makes a tax shelter

Tax havens are a popular, legal and often secret instrument for multinational corporations to move capital across borders. By taking advantage of loopholes in various national legislations and placing operations in countries with low taxes, companies can reduce their tax rate from around 35% to 25% to 15% or lower.

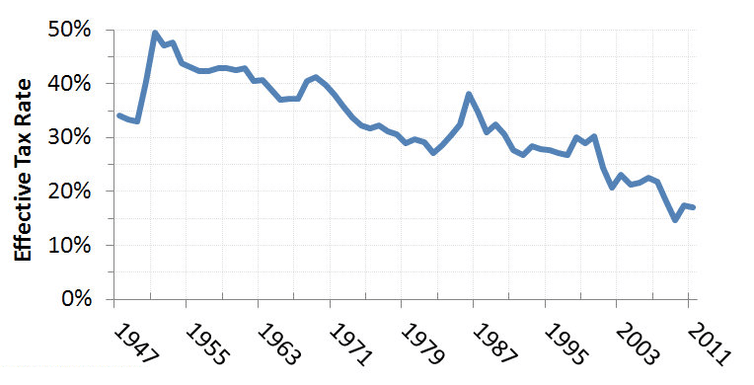

Figure 1: The United States Effective Corporate Tax Rate (1947-2011)

American companies use clever (and legal) tactics to offshore profits and reduce their tax burden. US Federal Reserve via Wikimedia

Silicon Valley companies have become expert at this tactic. Using a combination of subsidiaries in Ireland, the Netherlands and Bermuda to reduce its tax burden, Apple paid just 0.005% tax on its European profits in 2014, the European Comission reported.

If multinationals’ profits were accounted for where the economic activity takes place, they would pay a combined US$500 to US$650 billion more on taxes each year, according to estimates by the Tax Justice Network and the International Monetary Fund. Of this, around US$200 billion a year would go to developing countries, which is more than they receive annually in development aid (US$142.6 billion).

Findings like this have put tax havens on the radar of US and European regulators, but there’s no broadly accepted definition of what makes a country an offshore financial centre.

Lists published by the Organisation of Economic Cooperation and Development (OECD) and the International Monetary Fund use different criteria to define tax shelters, and their outcomes are highly politicised.

The Tax Justice Network’s Financial Secrecy Index, Oxfam’s list of the worst corporate tax havens and Jan Fichtner’s 2015 Offshore-Intensity Ratio have proven to be more useful.

Fichtner (a co-author of this article) provides a rough yardstick for judging OFC jurisdictions by examining the proportion between foreign capital, such as FDI, and the size of the domestic economy.

What none of these measures can tell us, though, is the origin of the foreign investment reported by these tax havens. How does Apple’s money get from California to Bermuda anyway?

Big data and network analysis

By bringing together political economists and computer scientists in the CORPNET research group at the University of Amsterdam, it became possible to study how corporations make use of particular countries and jurisdictions in their international ownership structures. The novel, data-driven network approach of our study shed light on how offshore finance flows across the globe.

We looked not at country-level statistics but at detailed company data. By asking which countries and jurisdictions play a role in corporate ownership chains that is incommensurate with the size of their domestic economies, we were able to identify, for the first time, a complex global web of offshore financial centres.

We analysed the entire massive global network of ownership relations, with information of over 98 million firms and 71 million ownership relations. This granular firm-level network data helped us to distinguish two kinds of tax havens: sinks and conduits.

Introducing sinks and conduits

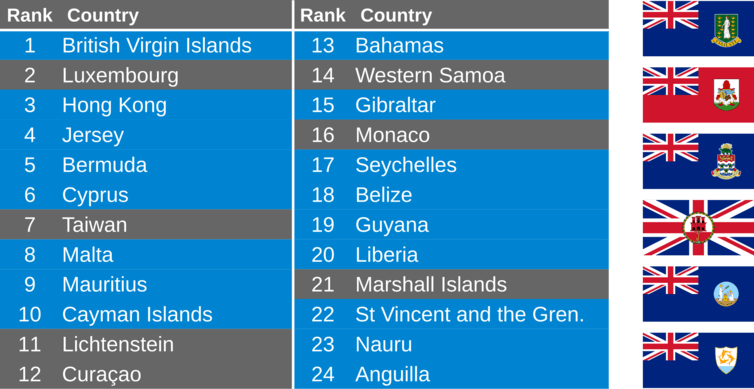

“Sink OFCs” attract and retain foreign capital. We identified 24 sink OFCs, including well-known tax havens such as Luxembourg, Hong Kong, the British Virgin Islands, Bermuda, and the Cayman Islands, but also Taiwan, a heretofore unnoticed tax haven.

Using our method, we can now investigate which jurisdictions are used by corporations en route to sinks. These “conduit OFCs” are attractive intermediate destinations because their numerous tax treaties, low or zero withholding taxes, strong legal systems and good reputations for enabling the quiet transfer of capital without taxation.

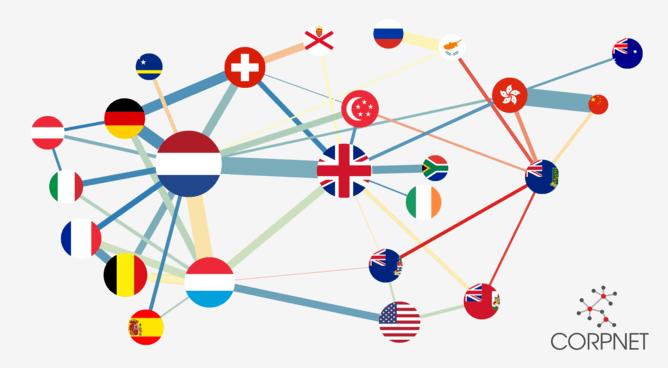

Figure 2: Mapping equity flows

The size of conduits (green) and sinks (red) reflects the investment that flows through the country. The colour to its position as a sink (blue = no sink, red = sink). The size of the arrows is proportional to the investment between two countries and the colour to its importance (blue = lower flow than expected, red = higher flow than expected). CORPNET

We found that a handful of big countries – the Netherlands, the UK, Switzerland, Singapore and Ireland – serve as the world’s conduit OFCs. Together, these five conduits channel 47% of corporate offshore investment from tax havens, according to the data we analysed.

The Netherlands leads the pack with 23%, followed by the UK (14%), Switzerland (6%), Singapore (2%) and Ireland (1%).

Each conduit jurisdiction is specialised both geographically and in industrial sectors. The Netherlands excels in holding companies, for example, while Luxembourg favours “administrative services”. Hong Kong’s geographic speciality lies in connecting to the British Virgin Islands and Taiwan.

New targets

Our findings debunk the myth of tax shelters as exotic far-flung islands that are difficult, if not impossible, to regulate. Many offshore financial centres are highly developed countries with strong regulatory environments.

That means that targeting conduit OFCs rather than sinks could prove more effective in stemming tax avoidance. This realisation may help European Union and the OECD officials, who have increased pressure on cracking down on tax avoidance since the 2008-2009 financial crisis (to modest effect), by helping regulators better tailor their policies.

British Finance Minister Philip Hammond has speculated that the UK could become a European tax haven if the EU fails to offer it a good Brexit deal. But, in practice, the City of London is already a major offshore financial centre.

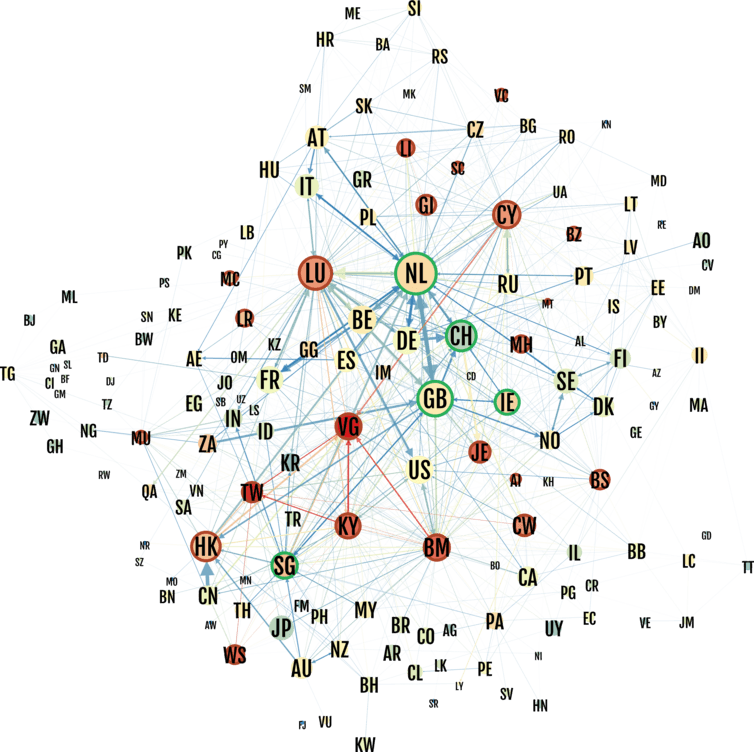

Figure 3: Sink Offshore Financial Centres

Jurisdictions in blue have been under British sovereignty in the past or are still UK dependencies. CORPNET, Author provided

Of 24 sink OFCs, 18 have a current or past dependence to the UK, including major tax havens such as the Cayman Islands, Bermuda, British Virgin Islands and Jersey. New territories with low or no corporate taxes are continuously emerging as sink OFCs, but, as our study shows, there are just a handful of conduit OFCs.

Results and details are available on the dedicated website www.ofcmeter.org

__________________________________________________

Javier Garcia-Bernardo – PhD Candidate, University of Amsterdam

Eelke Heemskerk – Associate Professor Political Science, University of Amsterdam

Frank Takes – Postdoctoral Researcher, University of Amsterdam, Leiden University

Jan Fichtner – Postdoctoral Researcher in Political Science, University of Amsterdam

Republish our articles for free, online or in print, under Creative Commons license.

Go to Original – theconversation.com

DISCLAIMER: The statements, views and opinions expressed in pieces republished here are solely those of the authors and do not necessarily represent those of TMS. In accordance with title 17 U.S.C. section 107, this material is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. TMS has no affiliation whatsoever with the originator of this article nor is TMS endorsed or sponsored by the originator. “GO TO ORIGINAL” links are provided as a convenience to our readers and allow for verification of authenticity. However, as originating pages are often updated by their originating host sites, the versions posted may not match the versions our readers view when clicking the “GO TO ORIGINAL” links. This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.